Source: Internet

Introduction

-

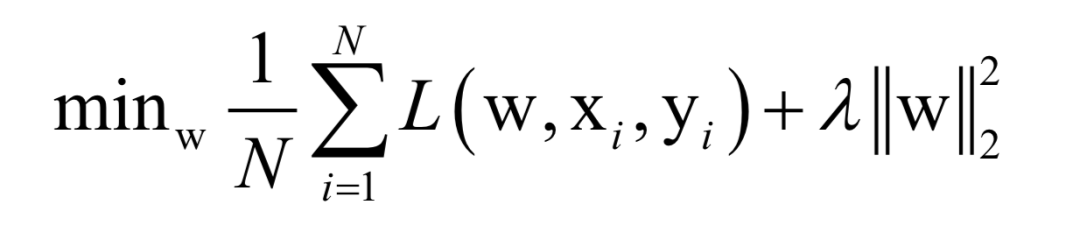

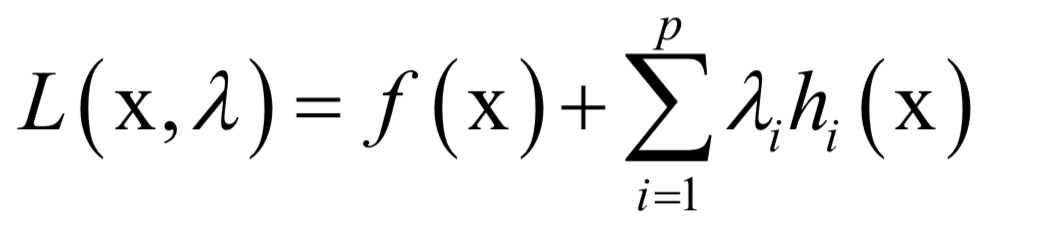

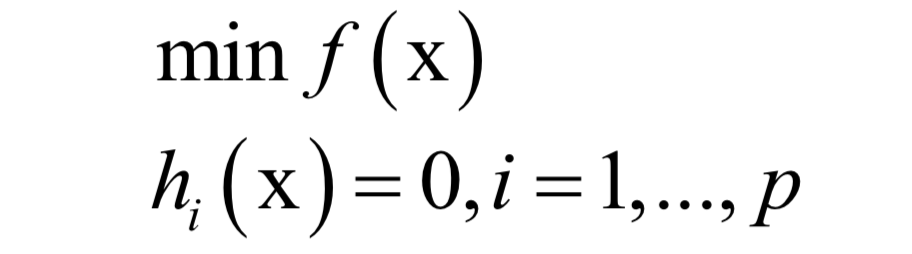

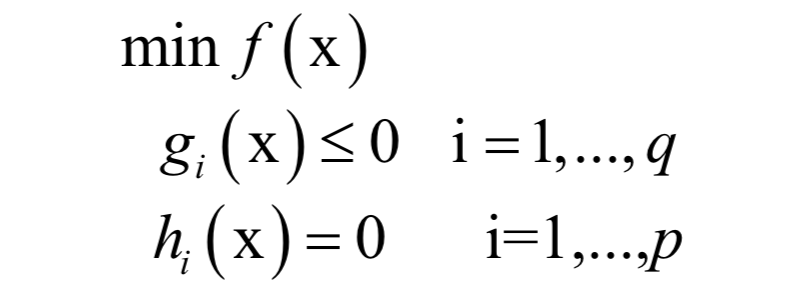

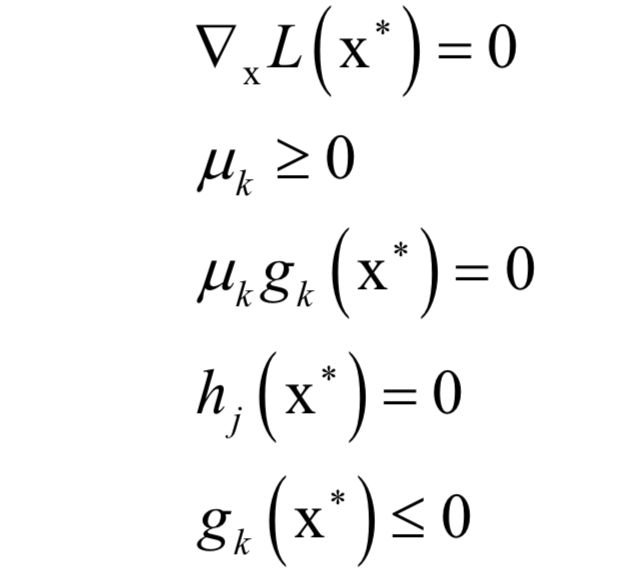

Analytical Solution

-

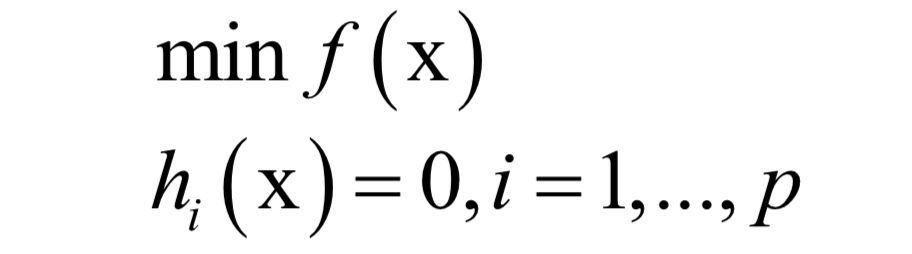

Numerical Optimization

-

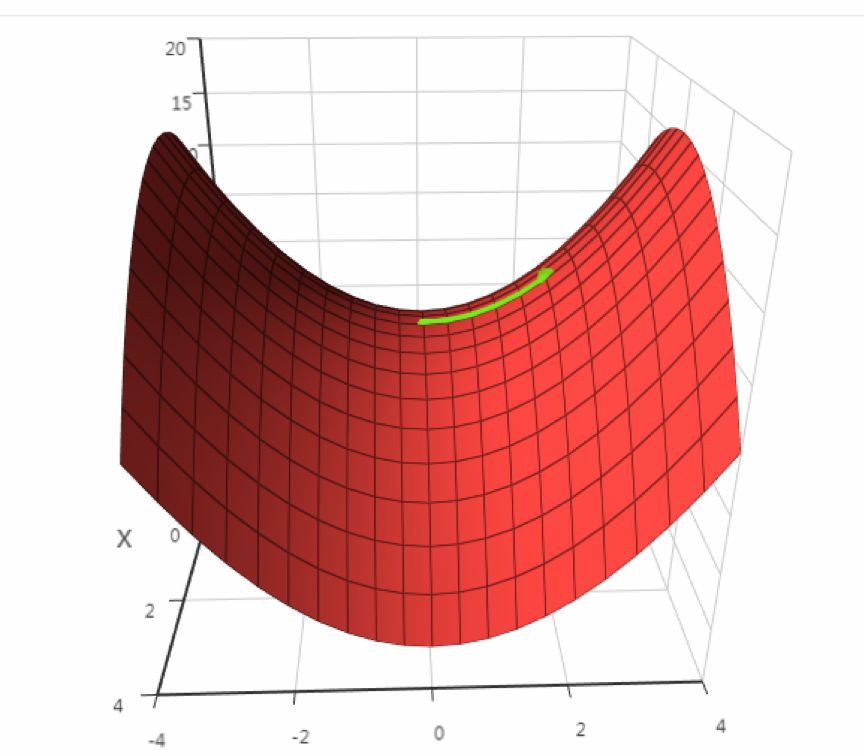

Can correctly find extreme points in various situations

-

Fast speed

-

If f”(x) > 0, then it is a minimum at that point

-

If f”(x) < 0, then it is a maximum at that point

-

If f”(x) >= 0, further examination of higher-order derivatives is needed

-

If the Hessian matrix is positive definite, the function has a minimum at that point

-

If the Hessian matrix is negative definite, the function has a maximum at that point

-

If the Hessian matrix is indefinite, further examination is needed (this part is incorrect)

-

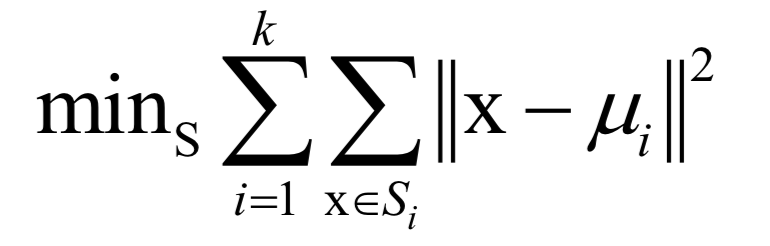

Principal Component Analysis

-

Linear Discriminant Analysis

-

Laplacian Eigenmaps in Manifold Learning

-

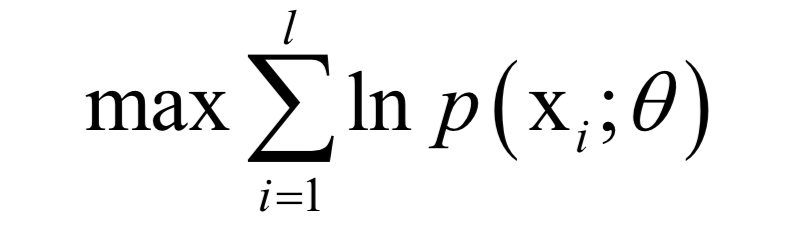

Hidden Markov Model

-

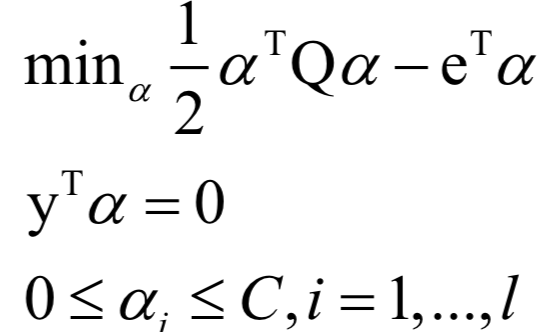

Support Vector Machine (SVM)

Editor / Fan Ruiqiang

Reviewed by / Wang Le

Checked by / Fan Ruiqiang

Click below

Follow us