Yesterday, OpenAI released what I believe is the most exciting product since ChatGPT – ChatGPT Operator. Since getting access to my account last night, I have been testing various tasks and quickly documenting some thoughts on this product in this article:

Operator and CUA Model – The Dawn of Agentic AI EraIn the previous public account article, I was still talking about AI Agents, and a few months later, Operator was released. This release marks a shift of AI from passive responses to active execution, based on the CUA model, which stands for Computer-Using Agent. By combining the multimodal capabilities of GPT-4o with RPA/simulated clicks, cloud hosts, and reinforcement learning, AI can interact with computer interfaces like humans. This means AI can not only understand and generate text but also complete complex tasks by “observing” the screen and “operating” the interface.

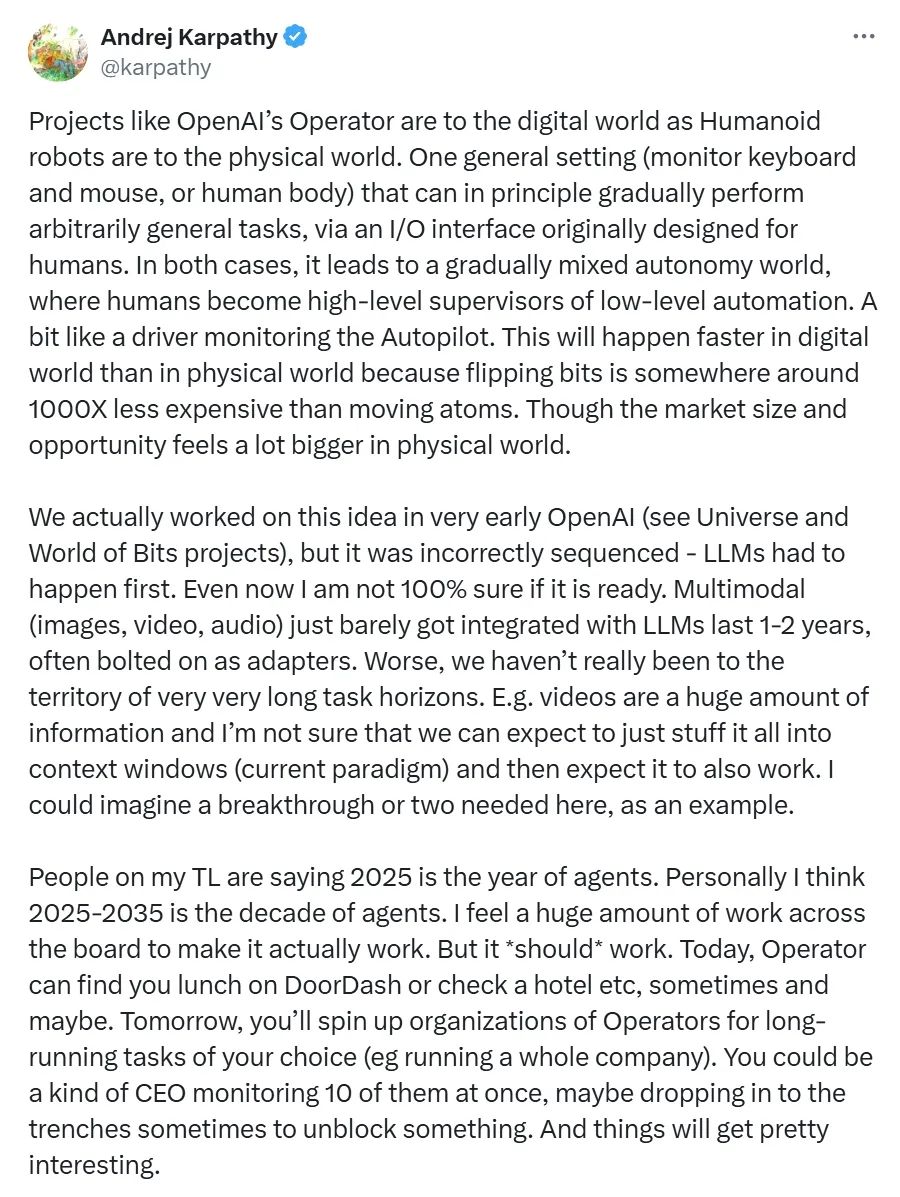

AI is transforming from information processing to information processing + task execution, opening up the generalization of AI Agents in various scenarios. This generalization will have a profound impact on various industries (RPA originally had no generalization capability), potentially leading to the disappearance of many traditional jobs while also creating many new opportunities. Here is a segment fromAndrej Karpathy’s X:

AGI’s Certainty in Future Computing Power Growth and StarGateNext, let’s talk about the controversial Stargate… So far, the most common question regarding the large-scale investment in AI has been about how to achieve commercialization. What is relatively certain now is that Agentic AI is the key path from the virtual world to AGI, while Embodied AI is the core channel from the physical world to AGI. LLMs have already opened the door for us to move towards AGI. As Agentic AI and Embodied AI continue to develop, and with the ongoing iteration of larger and better foundational models (Scaling Law remains effective), the demand for computing will continue to grow, and the certainty of investment in AI Data Centers will also increase.

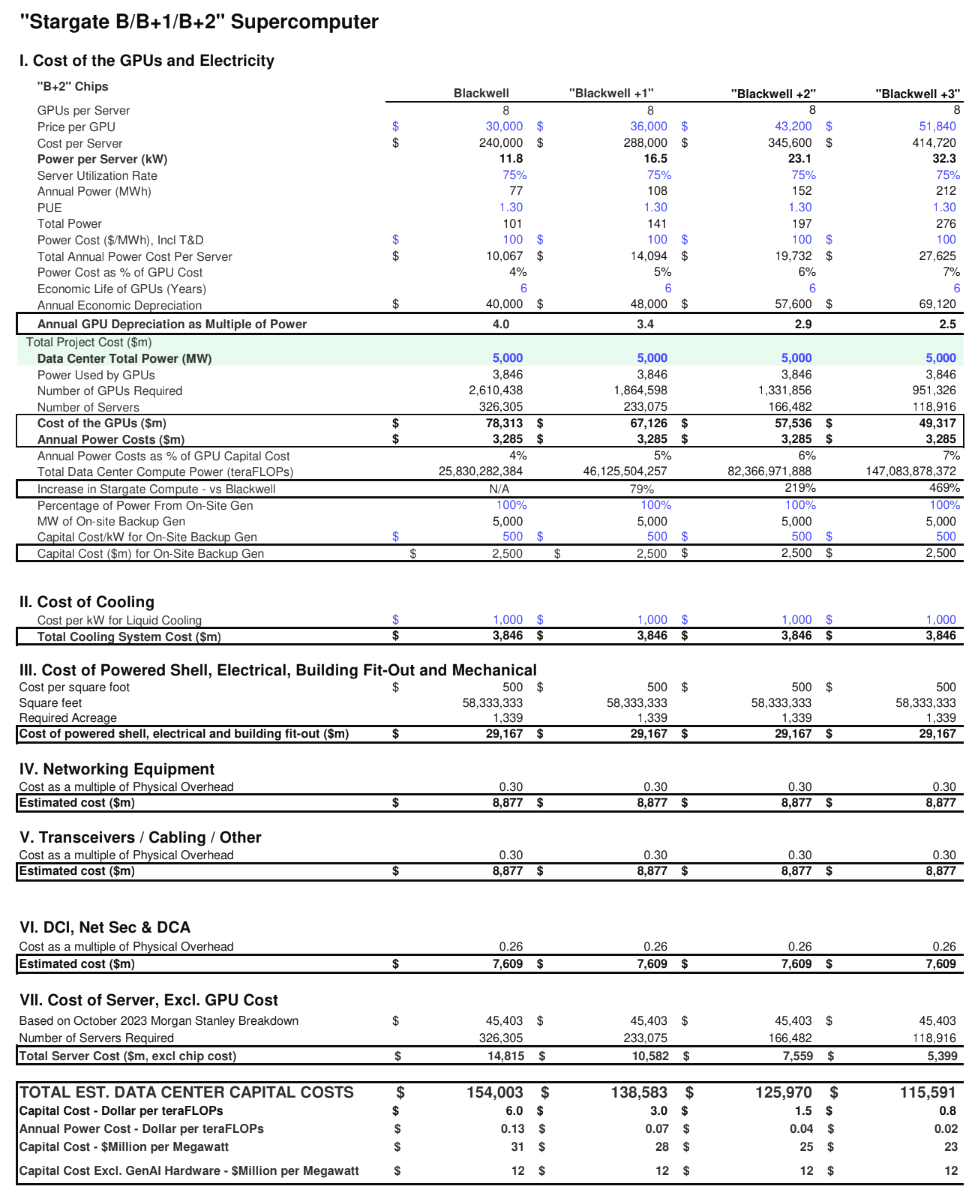

This week, OpenAI, SoftBank, and Oracle jointly announced an AI infrastructure project called “StarGate.” The project plans to invest $500 billion over the next four years to build a new generation of AI infrastructure (AI supercomputing centers), with an initial investment of $100 billion. The project aims to provide the necessary data and computing power for technologies like OpenAI’s ChatGPT.

Building AI supercomputing centers requires huge capital expenditures (CapEx), mainly for land, construction, GPUs, servers, and networking equipment. Operating costs (OpEx) mainly include electricity, labor, maintenance, and cooling. Typically, the construction cycle for data centers is 1-2 years, and after commissioning, revenue is generated by providing computing resources to AI companies, which takes another 12-18 months to reach full capacity. A rough calculation indicates that the next AI supercomputing center should break even within 5-8 years after reaching full capacity, while the average amortization of CapEx may take 8-10 years.

Although the total investment amount of $500 billion announced for the project has been questioned by many, the structure and financing details of the project are still being formulated. Both SoftBank and OpenAI have made it clear that they will each contribute only $15 billion, but many similar projects in the U.S. can leverage 1:3 to 1:5 from banks under a Power Purchase Agreement (PPA). So if the demand is there and the financial model is clear, the investment amount for the project can be realized. If this project can be built, it should significantly enhance Oracle’s position in the global Cloud market and SoftBank’s overall standing in the industry.

Finally, I want to say that AGI will create infinite possibilities, and we are standing at a historical turning point…