Author: He Shuchen, Product Marketing Head of the Direct Sales Division at Taikang Online Property Insurance Co., Ltd.

Source: “Insurance Theory and Practice” Volume 6, 2023

1. Introduction

With the arrival of the digital economy era, deep learning technologies are propelling artificial intelligence into a phase of large-scale application. Artificial intelligence is the main channel for future technological innovation and a fertile ground for nurturing world-class enterprises. On November 30, 2022, ChatGPT was launched, and within a week, it surpassed one million daily active users, reaching over one hundred million in two months, becoming a phenomenon in consumer AI applications. The content generation revolution sparked by ChatGPT has significantly impacted the financial industry, which inherently processes data and information. As a branch of the financial industry, the insurance sector focuses more on risk management and risk sharing, with the law of large numbers as its theoretical data foundation. Therefore, insurance companies are information-intensive enterprises. Currently, the insurance industry is at a critical transformation point, and the active application of ChatGPT technology by insurance companies will help accelerate the industry’s digitalization, assisting in the upgrade of organizational structures, business models, and internal processes to enhance service quality and efficiency. This is one of the important paths for the transformation of the insurance industry. Currently, experts in the insurance industry have reached a consensus that ChatGPT technology can first be applied in the fields of intelligent customer service and smart consulting. Therefore, this article explores the application of ChatGPT technology in insurance intelligent customer service.

2. The Journey of Information Technology and Knowledge Management in the Insurance Industry

(1) The Path of Information Technology in the Insurance Industry

The path of information technology in the insurance industry can be divided into four stages over time: before 2000 is the first stage, focusing on electronic construction; from 2001 to 2010 is the second stage, focusing on data centralization; from 2011 to 2022 is the third stage, focusing on data sharing; and after 2023 is the fourth stage, focusing on artificial intelligence construction.

From the industry perspective, the first stage of the insurance industry’s information technology journey was advocated and gradually standardized by government and regulatory departments, focusing on the electronicization of customer information, business information, and financial information, transitioning from manual operations to data information, ensuring data authenticity, effective archiving, and traceability. The second stage was led by government and regulatory departments, gradually constructing a supporting regulatory system for industry informatization. For instance, the China Insurance Industry Association was established in February 2001, and the Statistical Information Department of the China Insurance Regulatory Commission was prepared for establishment in 2003. In October 2004, the China Insurance Statistical Information System was put into use, and in July 2007, the insurance intermediary regulatory information system established by the Statistical Information Department began operation. In 2010, the industry vehicle insurance information central platform was established. The third stage was led by the industry regulatory system, promoting and participating in the gradual realization of data sharing within and across industries, including data sharing on insurance applications (application frequency, refusals, cumulative risk coverage) and claims (auto insurance, life insurance), as well as data sharing from other industries such as medical insurance (serious illness, benefit insurance) and medical institutions (innovative payment, insurance for pre-existing conditions). In June 2016, the first national-level, innovative insurance factor market, Shanghai Insurance Exchange Co., Ltd., was established and began operations in Lujiazui, Shanghai. In 2022, the insurance industry initiated research on the commercial insurance drug and device catalog. The fourth stage involves the extensive application of artificial intelligence, where issues such as overseas introduction of technology and data export, national security and data security, and management of sensitive information, as well as ethical issues related to information and big data, urgently require policy guidance from the industry regulatory system.

From the market entity perspective, the first stage of the insurance industry’s information technology journey was reflected in licensed institutions (insurance companies or insurance intermediaries) gradually popularizing office emails, portal websites, electronicization of paper documents, online business, and online finance, achieving collaborative office work among insurance headquarters, branches, subsidiaries, and various departments. The second stage was reflected in licensed institutions gradually achieving physical data centralization at headquarters, allowing headquarters to timely and comprehensively grasp the overall operational status of the company, branches, subsidiaries, and various departments, and make scientific decisions, transforming data information into data assets; enhancing risk management levels and operational efficiency, reducing corporate costs and risks, and improving profitability, beginning to seek a new direction centered on “customer-first.” The third stage was reflected in the arrival of the internet era, with business becoming mobile and scenario-based; licensed institutions began to reshape IT system architecture from the top down, transitioning from “passive construction” to “technology-led” to respond quickly to market demands. Group companies also achieved customer information sharing within the group, such as unified user IDs, unified portals (official websites, apps, and mini-programs), and data sharing and deep integration between business and finance. At the same time, the number of non-licensed institutions (mainly technology companies) increased. The fourth stage was reflected in some licensed institutions that, due to their first-mover advantage in science and technology, took the lead in implementing artificial intelligence projects, gradually embarking on differentiated development paths to achieve “overtaking on a curve.” For example, in February 2023, two insurance companies (Taikang Insurance Group and Beijing Life) announced their integration with Baidu’s “Wenxin Yiyan” and applied it in intelligent customer service, intelligent training, and other fields. Taikang Insurance Group also announced its collaboration with Baidu’s technical team to apply generative large model technology to emotional companionship for the elderly, sales assistance for agents, and intelligent training for agents, landing in the company’s core business scenarios to provide customers and sales teams with warmer, more standardized, and more intelligent services.

(2) The Path of Knowledge Management in the Insurance Industry

The concept of Knowledge Management (KM) was first proposed by Karl Wiig at the International Labour Conference of the United Nations in 1986 and has been nearly 40 years since. In 1996, the OECD’s “Knowledge-Based Economy” pointed out the indicator system of knowledge management and classified all human-created knowledge into four categories: the first category is factual knowledge (what), which belongs to narrative knowledge; the second category is principle knowledge (why), which belongs to natural principles and laws; the third category is procedural knowledge (how), which belongs to skills and abilities; the fourth category is knowledge about information and knowledge sources (who), which involves who knows and who knows how to do certain things. Among these, the first two categories are explicit knowledge, while the latter two categories are tacit knowledge. The OECD was the first official organization to use the concept of “knowledge economy” in international organizational documents. By 1999, 80% of American enterprises had implemented or were implementing knowledge management programs. In 2001, the World Bank pointed out in its report “China and the Knowledge Economy: Seizing the 21st Century” that “all economies are based on knowledge.”

Compared to the international market, China’s insurance industry started relatively late. In 1979, with the approval of the State Council, the People’s Insurance Company of China gradually resumed domestic insurance business, which had been suspended for over twenty years, bringing the financial term “insurance” back into the daily lives of Chinese people. In 1992, American AIA settled in Shanghai, introducing the individual agent system for life insurance marketing. Other insurance companies followed suit, introducing the individual agency system. It was not until the early 1990s that knowledge management began to be applied in the Chinese insurance industry.

Knowledge management is a crucial aspect of the daily operations of insurance companies, and the knowledge base system is an important part of the knowledge management system of insurance companies. Due to the strong professionalism, high accuracy requirements, the need for knowledge reasoning, complex business, and the broad scope of knowledge, as well as the unstandardized and low structured nature of data, the Q&A system between the insurance industry and ordinary consumers becomes particularly important. The knowledge base system, as the underlying support for the Q&A system, is one of the core competitive advantages of market entities in the insurance sector.

In recent years, leading insurance companies have made continuous investments and strategic upgrades in intelligent customer service. In 2019, Ping An Life launched the knowledge graph Q&A system called AskBob, fully utilizing the characteristics of knowledge graph’s hierarchical relationships, parallel similarities of entities, and reasoning of graph structures for better recall and more precise sorting. In 2021, ICBC-AXA Life proposed a knowledge management strategy and invested in building a knowledge management system with functions including business knowledge maps, knowledge search, knowledge content management, publication review management, knowledge security and permission management, and knowledge asset and usage statistics management. In 2022, China Life built an intelligent dialogue analysis platform based on the high-frequency business scenarios of 95519 and massive customer contact data, establishing semantic analysis capabilities and creating a smart ecological service for customer contact that includes reminders before, assistance during, and follow-ups after interactions, aimed at customers, agents, and management personnel. In 2022, AIA Life’s official website supported consumers in accessing its knowledge base through Baidu speakers to query insurance knowledge. In 2022, ZhongAn Insurance independently developed an innovative, full-stack digital customer service solution featuring “human-machine integration” and “full-cycle closed-loop” capabilities, achieving four major functional scenarios: first, human-machine collaboration to handle complex, high-concurrency service scenarios; second, combining differentiated and standardized services to stratify customer groups; third, solidifying standardized customer service (SOP) to support real-time maintenance and updates of the knowledge base; fourth, achieving traceability of service history and trackability of service quality, with point-to-point quality inspections and end-to-end complaint process follow-ups.

China’s economy has entered the “service economy” era, and the ability to maintain smooth communication with users is the key to winning in market competition. Intelligent customer service has gradually become one of the core competitive advantages of market entities in the insurance sector.

(3) The Application Journey of AIGC in the Insurance Industry

When discussing insurance intelligent customer service, one cannot ignore the recent popular technology, ChatGPT. Artificial Intelligence Generated Content (AIGC) refers to a new type of technology that uses artificial intelligence to automatically generate content, including text, images, audio, video, and code. Among the modalities of AIGC technology applications, text generation is one, and ChatGPT is one of the representative products of text generation.

ChatGPT (Chat Generative Pre-trained Transformer) is a natural language processing tool driven by artificial intelligence technology developed by the American AI research company OpenAI, released on November 30, 2022, causing a global sensation. ChatGPT is also known as an AI chatbot program that can engage in dialogue by understanding and learning human language, interact based on the context of the chat, and perform tasks such as writing emails, video scripts, copywriting, translation, coding, and academic papers, just like a human.

During the World Economic Forum held in Davos, Switzerland in 2023, Microsoft CEO Satya Nadella engaged in a conversation with Wall Street Journal editor Matt Murray, where Nadella stated that the impact of ChatGPT technology is comparable to the Industrial Revolution, and the development in the field of artificial intelligence can currently be described as “exponential.”

In 2023, Baidu’s founder, chairman, and CEO Li Yanhong stated in an internal letter: “The emergence of generative AI and large models is a new opportunity brought by a new computational paradigm. This means that AI technology has reached a critical point, and all industries will inevitably be changed. The Chinese AI market is about to experience explosive demand growth, and the release of its commercial value will be unprecedented and exponential… Humanity has entered the era of artificial intelligence, and the technology stack of IT has undergone fundamental changes. In the past, it was basically divided into three layers: chip layer, operating system layer, and application layer. Now it can be divided into four layers: chip layer, framework layer, model layer, and application layer.

In 2023, the Jiazi Guangnian Think Tank also predicted that the current technology stack still cannot meet the new generation of AI wave driven by ChatGPT, and the future AI technology stack will present a new technological architecture system. In the future, there will be an intermediate layer formed between the foundational models and specific AI application development, connecting to large model capabilities below and providing personalized services above.

The market entities in the insurance industry consist of licensed and non-licensed categories, with licensed institutions including insurance companies and insurance intermediaries, while non-licensed institutions are mainly insurance technology companies. Among them, insurance companies are divided into traditional insurance companies and specialized internet insurance companies. AIGC technology will impact various market entities within the insurance industry ecosystem, especially in the field of internet insurance.

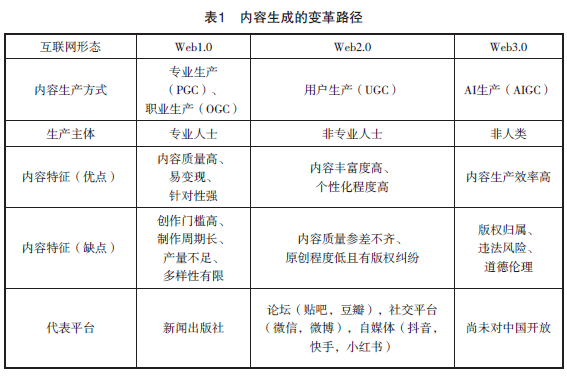

The role of internet technology in the insurance industry can be divided into three stages over time. Before 2018, insurance companies empowered insurance products and services through internet technology: designing scenario-based, fragmented, and high-frequency insurance products, such as e-commerce return insurance and flight delay insurance; optimizing service experiences, such as rapid claims, intelligent Q&A, and smart insurance consulting. From 2018 to 2022, insurance companies empowered insurance channels and customers through big data technology: assisting channels in accurately reaching specific customer groups, enhancing customer acquisition capabilities, and reducing acquisition costs, such as scenario embedding, user profiling, and precision marketing; empowering customers to enhance their consumption interest, such as retention on policy cancellation, add-on purchases, and repurchases. After 2023, insurance companies will empower digital content creation through internet technology. With the development of AIGC in text, audio, video, and image content generation, the world will gradually become content-driven, and the contentization of internet insurance will also accelerate, having already experienced three stages: Professional Generation (PGC) and Occupational Generation (OGC), User Generation (UGC), and AI Generation (AIGC). Each has characteristics defined by originality, content quality, and update frequency in an impossible triangle.

In the PGC and OGC stages, the content of internet insurance was primarily produced by industry professionals with certain knowledge and professional backgrounds, while ordinary consumers (internet users) mainly listened and watched. In the UGC stage, on one hand, internet users contributed ideas and injected fresh blood and vitality into internet insurance operations; on the other hand, they also supervised insurance institutions, advocating for democratic governance in the insurance industry. In the AIGC stage, due to the rapid democratization of content tools, the competition in internet insurance will evolve into a content battle, namely a technological competition of AIGC, where internet users adept at applying AIGC technology will dominate the discourse, while those who do not will have their discourse power weakened.

As AIGC technology transforms the way and efficiency of digital content generation, “monetizing imagination” is becoming a new business. AIGC technology can be applied in the insurance industry in the following scenarios:

(1) Virtual AI anchors: breaking through the bottleneck of anchor cultivation, reducing marketing costs for internet insurance;

(2) Virtual AI customer service: improving the efficiency of knowledge dissemination and knowledge accumulation, lowering service costs for internet insurance;

(3) AI intelligent insurance consulting: uncovering consumer insurance needs, enhancing user management efficiency;

(4) Digital companionship: reducing the incidence of psychological disorders in specific customer groups, such as adolescents, pregnant women, and elderly individuals living alone;

(5) AI consultations, AI medication advice, and medication reminders: lowering the value-added service costs for insurance companies, enhancing user service experiences;

(6) AI knowledge popularization in health and medicine: improving the professionalism of popular science, enriching agents’ social media content, reducing customer complaints, and enhancing customer satisfaction;

(7) AI intelligent marketing: enhancing efficiency and effectiveness in sales processes such as lead discovery, customer outreach, and customer conversion, customizing customer solutions to improve conversion rates and sales.

ChatGPT has unlocked image recognition capabilities, enabling AI to interpret natural language and visual information, making AI more like a person with “eyes” and “language” abilities, broadening the capabilities of insurance intelligent customer service to interact with users and creating more opportunities. China’s economy has entered the “service economy” era, and the ability to maintain smooth communication with users is the key to winning in market competition. Intelligent customer service, as a bridge connecting insurance companies and users, is undeniably important.

3. The Application of AIGC in Intelligent Customer Service in the Insurance Industry

The informatization of the insurance industry can enhance the overall management efficiency of the insurance sector, making information exchange within the industry more standardized, transparent, and traceable. However, the informatization of the insurance industry also faces multiple pain points, such as poor data quality, severe information distortion, and information silos. Poor data quality arises from human errors or business misconduct, leading to the input of large amounts of garbage data into the system, resulting in low authenticity, completeness, comprehensiveness, and usability of foundational data. Severe information distortion is due to personnel misunderstandings or system incompatibilities, causing information to be fragmented, filtered, imagined, or altered, leading to transmitted information deviating from the true situation or measurement standards. The prevalence of information silos is often due to weak planning in informatization construction, where business, product, financial, and other systems operate independently and do not interconnect, reducing the efficiency of data processing and the quality of data assets.

The knowledge base of insurance companies is an important carrier of informatization and knowledge management in the insurance industry. During its construction process, it faces three pain points: strong professionalism, high accuracy requirements, and the need for knowledge reasoning. Strong professionalism is reflected in the abundance of insurance knowledge and professional terms; some words may have a high degree of literal or semantic matching but represent different meanings in the insurance industry, thus making text matching methods based on literal or semantic matching difficult to meet the needs. High accuracy requirements are due to strict underwriting, policy maintenance, and claims rules within insurance companies; inaccurate responses can lead to significant economic losses for users and generate numerous customer complaints. The need for knowledge reasoning arises because user inquiries in the insurance industry often involve medical or industrial terms from other fields; relying solely on insurance knowledge cannot resolve user questions, necessitating extensive medical and industrial knowledge for problem reasoning and answer selection.

The knowledge base of insurance companies is core to intelligent customer service, and its pain points lead to four issues in intelligent customer service: difficulty in communication, lack of specialization in service, immature underlying technology, and high costs. Difficulty in communication is evident as intelligent customer service can easily handle repetitive structural issues. However, the varying ways users phrase questions and structure sentences often lead to intelligent customer service being unable to accurately understand the true meaning of questions, affecting user experience. Lack of specialization in service is evident as insurance users expect more targeted and human-centered customer service, yet the service processes and scripts of intelligent customer service exhibit standardization, failing to capture changes in user emotions sensitively, creating a gap in emotional connection between users and enterprises. Immature underlying technology is reflected in the fact that while both the state and the market actively promote the research and development of artificial intelligence technology, the lengthy R&D cycle and the asynchrony between technology research and transformation still leave significant room for improvement and breakthroughs in the underlying technology of artificial intelligence. High costs are due to the customized nature of intelligent customer service solutions, determined by the enterprise’s development status and the business logic and core pain points of the industry. This also indicates that the reusability of technology across different enterprises and industries is low; the barriers to technology transfer lead to higher overall costs for suppliers.

Compared to traditional insurance business, intelligent customer service is even more crucial for internet insurance companies. This is because internet insurance companies typically have lower average premiums per policy and higher average service costs for customers, making it challenging to reduce costs and enhance operational efficiency, which in turn restricts improvements in customer experience. Furthermore, internet insurance often involves less direct communication with customers during marketing, leading to issues such as insufficient explanation of insurance contract terms and misunderstandings by customers, resulting in high complaint rates that affect policy renewals and customer management. High-quality intelligent customer service can effectively address these two pain points in the internet insurance industry, lowering operational costs and complaint rates, and enhancing brand image and profitability.

The application of AIGC in intelligent customer service in the insurance industry should not only focus on upgrading IT technology (algorithms and computing power) but also emphasize the “human” aspect, particularly the collaboration efficiency between the insurance business team and the IT technology team.

First, organizational structure and job responsibilities need to be clear and defined. Intelligent customer service represents the insurance company in facing a massive user base, including internal employees, management, and external consumers, and must provide accurate and timely information for all aspects of the insurance company’s operations. If the organizational structure and job responsibilities are unclear, patchwork solutions or temporary corrections will not only be costly but also inefficient and ineffective.

Second, daily information updates or iterations need to become standardized work processes. Insurance companies generate a massive amount of information updates and iterations daily, requiring timely deletion of redundant information. For industry-level general knowledge, dedicated personnel must be responsible for inputting various knowledge, concepts, cases, and relationships within the insurance industry to ensure authenticity, accuracy, completeness, and timeliness. For company-level business knowledge, dedicated personnel must summarize high-frequency keywords, matching relationships, and other elements that facilitate information structuring, to promptly update newly launched products or services, new channels or business scenarios, and the daily interactions of massive users. Additionally, dedicated personnel must be responsible for real-time deconstructing and iterating this information into the customer service system. Only after addressing these issues can discussions about IT technology aspects, such as the implementation of AIGC in intelligent retrieval and intelligent Q&A functions and computing power issues, take place.

Third, close communication with IT staff regarding business needs is essential. For example, the demands for insurance business data analysis and mining need to be detailed and clear, specifying which fields should be displayed in data visualization and business analysis reports, and the format of display. Furthermore, the requirements for the interplay between human and AI work must be detailed and clear: when should user inquiries be transferred to human agents? How should the workflow of tickets or hotlines be managed in terms of timeliness? How can the knowledge be updated and ensured for accuracy?

Finally, AI also has the capability to provide users with appropriate emotional value. Therefore, insurance company staff should enhance emotional training for personnel, such as enabling AI to automatically analyze the intent behind user questions and provide optimal answers, achieving intelligent Q&A functionality; AI can sense changes in user emotions and provide appropriate emotional responses.

Of course, the commercial use of AIGC technology in the domestic financial industry may still face some uncertainties, such as the overseas introduction of artificial intelligence technology and its stability, national security and sensitive information management, and ethical issues related to information and big data. These all await clear policy guidance from regulatory authorities.

4. Conclusion

After 2023, the informatization of the insurance industry will primarily focus on artificial intelligence construction, and the role of internet technology in the insurance industry will shift to empowering digital content creation. This requires government and regulatory departments to provide policy guidance and clarify the legal and compliance boundaries for the commercial application of AIGC technology. At the same time, all insurance companies should recognize the positive impact of ChatGPT and AIGC technology on the informatization and digitalization of the insurance industry. Those who can effectively utilize this technology will dominate content generation and gain greater discourse power through internet platforms, achieving “overtaking on a curve.”

China’s economy has shifted from an “industrial-led” model to a “service-led” model, entering the “service economy” era. The ability to maintain smooth communication with users is the key to winning in market competition. Intelligent customer service has gradually become one of the core competitive advantages of market entities in the insurance industry.

Reprinted from: China Insurance Society